What three services do most financial institutions typically offer?

Today, most large banks offer deposit accounts, loans, and limited financial advice to both consumers and businesses. Products offered at retail and commercial banks include checking and savings accounts, certificates of deposit (CDs), personal and mortgage loans, credit cards, and business banking accounts.

Banks, Credit Unions, and Savings & Loans

These financial institutions accept deposits and offers checking and savings account services; make business, personal, and mortgage loans; and provides basic financial products like certificates of deposit (CDs).

All services related to money are considered financial services. Banking, mortgages, credit cards, payment services, tax preparation and planning, accounting, and investing are types of financial services industries. Financial services are frequently the exclusive domain of businesses and professionals.

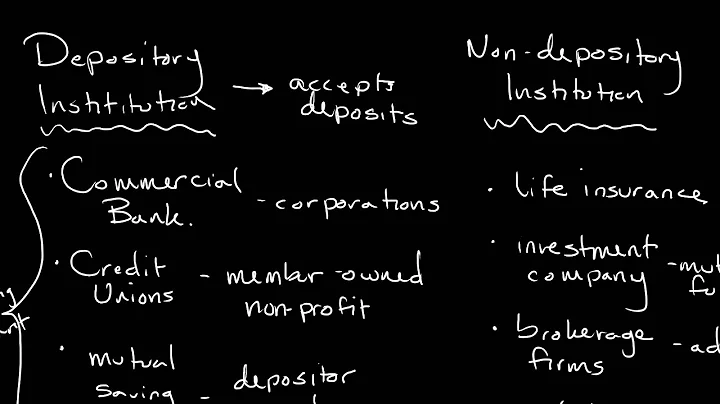

They are commercial banks, thrifts (which include savings and loan associations and savings banks) and credit unions. These three types of institutions have become more like each other in recent decades, and their unique identities have become less distinct.

All financial institutions usually offer basic banking services (checking and savings accounts, consumer loans, etc.) with larger ones offering a fuller range of services (credit cards, mortgages, foreign currencies, etc.).

- Checking Accounts. An account at a financial institution that allows for withdrawals and deposits. ...

- Savings Accounts. ...

- Money Market Accounts. ...

- Certificates of Deposit. ...

- Mortgages. ...

- Home Equity Loans. ...

- Auto Loans. ...

- Personal Loans.

Securities are fungible and tradable financial instruments used to raise capital in public and private markets. There are primarily three types of securities: equity—which provides ownership rights to holders; debt—essentially loans repaid with periodic payments; and hybrids—which combine aspects of debt and equity.

Banks are undoubtedly the most recognized and familiar financial institutions. They offer numerous services to customers, including checking and savings accounts, loans, credit cards, and investment services. Banks are federally regulated, which ensures that they operate in a safe and compliant manner.

Banks are the most common financial institution because they offer the most financial services. Checking accounts, savings accounts, home loans (mortgages), car loans, student loans, investment advice, ATMs, direct deposit and foreign currency swaps are just some of the many services banks offer.

There are three main types of financial institutions: banks, credit unions, and savings and loans.

What is the 3 financial statement practice?

In financial modeling, the “3 statements” refer to the Income Statement, Balance Sheet, and Cash Flow Statement. Collectively, these show you a company's revenue, expenses, cash, debt, equity, and cash flow over time, and you can use them to determine why these items have changed.

The 5 most important banking services are checking and savings accounts, loan and mortgage services, wealth management, providing Credit and Debit Cards, Overdraft services. You can read about the Types of Banks in India – Category and Functions of Banks in India in the given link.

The “big four banks” in the United States are JPMorgan Chase, Bank of America, Wells Fargo, and Citibank. These banks are not only the largest in the United States, but also rank among the top banks worldwide by market capitalization, with JPMorgan Chase being the most valuable bank in the world.

They earn interest on the securities they hold. They earn fees for customer services, such as checking accounts, financial counseling, loan servicing and the sales of other financial products (e.g., insurance and mutual funds).

Fifth Third Bank (5/3 Bank), the principal subsidiary of Fifth Third Bancorp, is an American bank holding company headquartered in Cincinnati, Ohio.

- Checking accounts.

- Savings accounts.

- Debit & credit cards.

- Insurance*

- Wealth management.

But compared to banks, credit unions tend to be smaller, operate regionally and are not-for-profit. In many instances, they offer lower rates on loans, charge fewer fees and offer better interest rates for deposit accounts than traditional banks.

- Traditional Checking Account. A traditional checking account, also referred to as a standard or basic checking account, offers the ability to write checks. ...

- Premium Checking Account. ...

- Interest-Bearing Checking Account. ...

- Rewards Checking Account. ...

- Student Checking Account. ...

- Second Chance Checking Account.

What are the three main categories of services offered by financial institutions? These are savings, payment services, and borrowing.

The primary role of banks is to take deposits and make loans. But banks can offer a wide range of products and services, including: Deposit accounts (checking accounts, savings accounts, CDs, money market accounts) Loans, including mortgage loans, auto loans and personal loans.

Which financial institution only provides services for its members?

Credit unions operate to promote the well-being of their members. Profits made by credit unions are returned back to members in the form of reduced fees, higher savings rates and lower loan rates.

The two main types of financial markets are Capital Markets and Money Market. The capital market is the market for medium and long term funds. You can read about the Financial Market – Functions, Features, Difference between Money and Capital Market in the given link.

Stocks, bonds, preferred shares, and ETFs are among the most common examples of marketable securities. Money market instruments, futures, options, and hedge fund investments can also be marketable securities.

What are the Types of Security? There are four main types of security: debt securities, equity securities, derivative securities, and hybrid securities, which are a combination of debt and equity. Let's first define security.

The Short Answer: Yes. Share: The IRS probably already knows about many of your financial accounts, and the IRS can get information on how much is there. But, in reality, the IRS rarely digs deeper into your bank and financial accounts unless you're being audited or the IRS is collecting back taxes from you.